Your Right to Terminate Due to Lender's Appraisal

Good morning, and welcome! The Addendum Concerning Your Right to Terminate Due to Lender's Appraisal, is a document with three options that can change your ability to terminate the sale contract because of an appraisal. Here are a few things you should know about the document and why you may ask your Realtor if it is in your best interest to complete one.

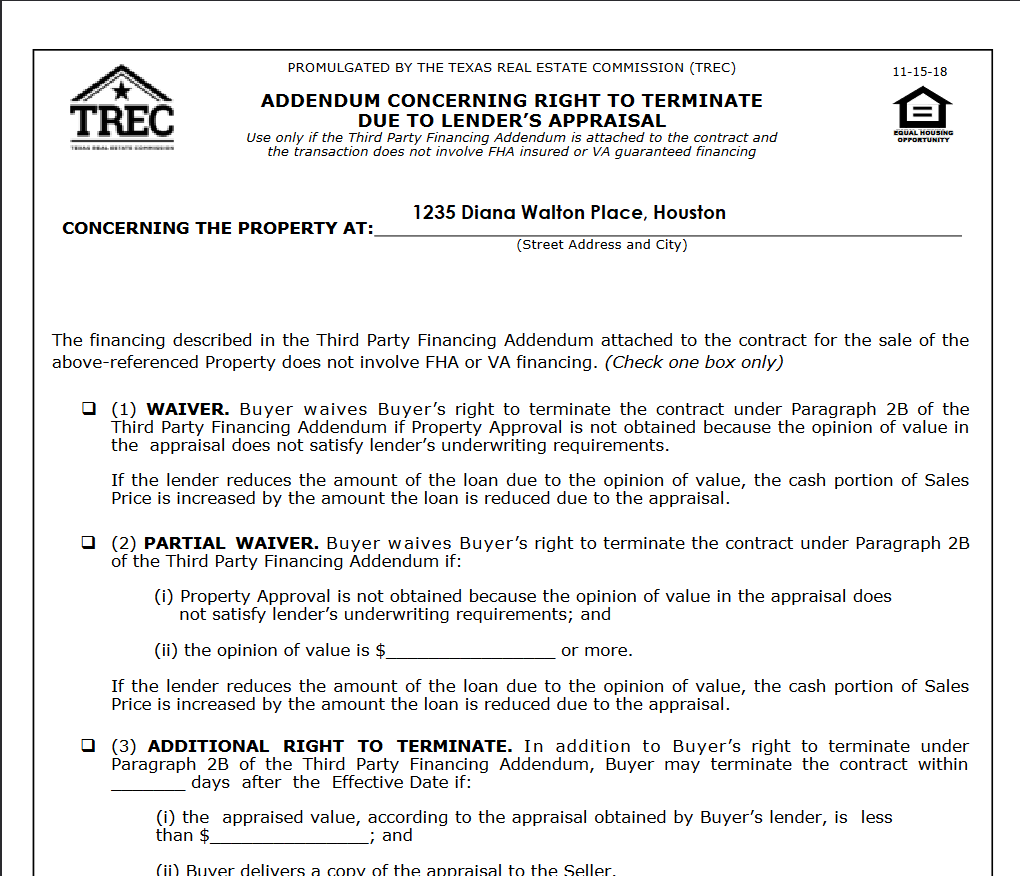

- The Addendum Concerning Right to Terminate Due to Lender’s Appraisal is to be used only when the Third-Party Financing Addendum is used.

- It cannot be used if you are a cash buyer, or using a VA or FHA loan product.

- Document must be submitted with the contract.

- The document gives you three options that can affect your ability to terminate the sale contract due to appraisal issues.

- If you choose option 1, you waive your right to terminate the contract under paragraph 2B of the Third Party Financing Addendum, regardless of how low the property appraises.

- Option number 2, while you will be waiving your right here as well if the appraisal does not meet the lender's underwriting requirements, under this option, you can agree on a limit of how low the appraisal must be for the to waiver applies. For example, if the appraisal is equal or greater than the amount in line 2(ii) the waiver applies and you cannot terminate. However, if the appraisal is lower than the amount written in 2(ii) the waiver will not apply and you can terminate.

- Option 3, states, in addition to your right to terminate under Paragraph 2B of the Third Party Financing Addendum, you may also terminate the contract within X number of days after the effective date if the appraised value is less than X, which should be filled in line 3(i) and a copy of the appraisal is delivered to the seller along with notice of termination.

- The document will require both the buyer's and seller's signatures.

While this addendum is not required or necessary if you are not interested in modifying your right to terminate due to the lender's appraisal, if you believe the appraisal will be an issue, you should speak with your Realtor. Also, discuss the options with your Realtor, as well as any possible financial consequences relating to those options. In addition, when selecting an amount for line 2(ii) or line 3(i), make sure to discuss the amount with your Realtor and do not forget to choose an amount you will be comfortable with to avoid financial strain.

If it matters to you, it matters to us. We are always looking out for your best interest. As always, thank you so much for stopping by, and remember, if you are thinking of purchasing your new home, or selling an existing one, please give us a call. We are here to help. We have been helping home buyers and sellers 12 years and counting. Until next time...Diana

Source: Bankrate

Image by Diana Walton

Astor & Eaton Realty

Diana Walton

Real Estate Broker

713.208.8013

Write to Diana Walton at homes@astoreaton.com

https://www.har.com/dianawalton

We do more because we care more