What Affects Mortgage Rates? Understanding Real Estate

Watch the video instead

Have you ever wondered what drives mortgage rates?

In short, two things: 1) the Federal Reserve and 2) (these are the biggest things to watch) 10-year Treasury Yields.

1. The Federal Reserve

The nation's central bank raises and lowers the interest rate at which banks lend to each other overnight as a tool to strike a balance between too much economic growth, which drives up inflation, and too little growth, which can trigger a recession and cause wide-spread unemployment.

In tough times, like the pandemic, low rates encourage purchasing and keep the economy moving forward. When the economy picks up and things start getting too expensive, inflation becomes a concern so they raise interest rates to make borrowing more costly in an effort to slow things down.

The rise and fall of those rates eventually impacts home buyers.

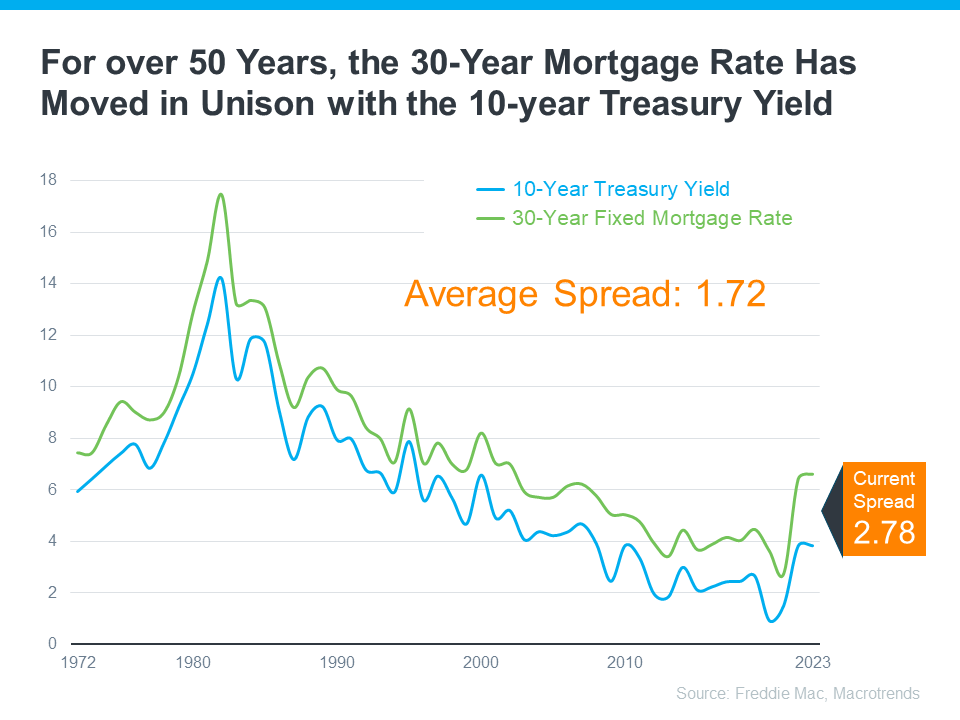

2. 10-year Treasury Notes

The 10-year Treasury note is a 10-year loan given by the public to the U.S. government. In return, the government pays investors a fixed amount of interest every six months.

Mortgage-backed securities (ownership interest in a pool of mortgage loans) play a game of follow-the-leader with the 10-year Treasury note because they are both in competition for investor money. If Treasury rates are low, it's like a sale on borrowing money. Mortgage rates tend to follow; they also go down. If Treasury rates rise, it's like a signal for mortgage rates to go up too.

Want to stay ahead of the game?

Keep an eye on the 10-year Treasury yield curve. By checking out current and past rates, you can get a sense of where fixed mortgage rates might be headed.

Stay informed and happy house hunting!

If you have any other real estate-related questions, reach out to me; I'd love to help.