Boost Credit Score for a Strong Mortgage Application

Are you gearing up for your homebuying journey? Well, you most probably need home financing, right? So, how can you make your mortgage application worthy enough for approval? By indicating your financial responsibility and ability to repay debt, your credit score is, undoubtedly, a major factor that makes your application stronger. Although it is not the ONLY factor, it is still a major one in determining your mortgage eligibility.

So, your application approval may depend on whether or not you meet the required credit score. Don't worry if you don't! By keeping a check on your credit utilization ratio and employing actionable strategies and expert tips, you can enhance your creditworthiness.

From understanding the factors that influence your score to implementing effective credit management techniques, let's unravel the secrets of boosting your credit score to strengthen your mortgage application. Let's maximize your credit score's potential!

Key Takeaways

- A strong credit score is crucial for a successful mortgage application, as it demonstrates your financial responsibility and repayment capability.

- Strategies for boosting your credit score include checking your credit report for errors, paying bills on time, reducing debt, avoiding new credit applications, keeping credit accounts open, and maintaining a diverse credit mix.

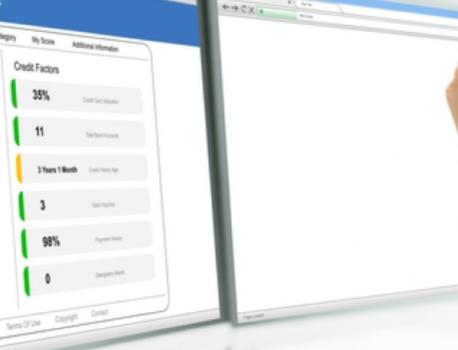

- Regularly monitor your credit score using free services like Credit Karma or Credit Sesame.

- The time it takes to improve your credit score varies depending on your financial history and actions, but patience, effort, and consistency are key.

- Beware of credit repair companies and debt settlement firms that may promise quick fixes but can potentially harm your credit further.

- By proactively managing your credit score and credit utilization ratio, you can strengthen your mortgage application and potentially secure better loan terms and interest rates.

Strategies to Bring a Boost to Credit Score

Let's dig in to learn the smart techniques and how to implement effective tactics to elevate your credit score and enhance your financial standing.

- Credit Report Check-up

To begin enhancing your credit score, spare some time to review your credit report. Your credit report encompasses details concerning your credit background, such as your credit accounts, payment records, and any unsettled debts.

Are you now thinking about how you can access your report? The three primary credit bureaus (Equifax, Experian, and TransUnion) give you a chance to obtain a complimentary copy of your credit report once annually through the website AnnualCreditReport.com. Nice, isn't it?!

Meticulously reviewing it for any errors or inaccuracies is your responsibility though. DO THAT! Any inaccurate information otherwise may impact your credit score or credit utilization ratio.

Now let's suppose, during your review, you come across any errors, what should you do then? You need to dispute the inaccuracies with both the credit bureau and the creditor responsible for reporting the erroneous information immediately. Get the rectification done quickly to evade any harm to your mortgage application!

Now let's suppose, during your review, you come across any errors, what should you do then? You need to dispute the inaccuracies with both the credit bureau and the creditor responsible for reporting the erroneous information immediately. Get the rectification done quickly to evade any harm to your mortgage application!

- Bill Payment Promptness

Paying your bills without crossing the deadlines is not just a good habit but also is too big a factor to ignore due to its huge impact on credit score. Remember your payment history weighs the highest when your credit score is being computed!

Obtain more benefits than just late fees and penalties by making timely payments. Wondering what benefits? Dodging the damage to your credit score!

If your mind is enjoying the thoughts of such benefits but you have a short memory and worry about how to make all this happen, don't panic! Simply set up automatic payments or reminders and stop missing any due payments

Another important point to keep in mind is that late payments remain recorded on your credit report for up to seven years, so it's important to avoid them whenever possible. Get your delinquent accounts cleared!

Learn More:

Calculate Your Monthly Mortgage- Debt Conquering & Credit Utilization Ratio Optimization

Your credit utilization ratio is like a skilled tightrope walker, delicately balancing your outstanding balances and credit limits to achieve financial harmony. If you would disturb that balance, the tilt of your ratio would bring a dip in your credit score. Certainly, what you do not want!

So, pay down your debts and avoid taking up extra credit, especially when you are going to apply for a mortgage. Maintaining your credit utilization ratio below 30% would take you to places when it comes to your application approval.

Where to start? Is this the question in your mind now? You can start by paying off high-interest credit card debts, and then work your way down to lower-interest debts.

- Cap on the New Credit Application

Each time you seek out fresh credit opportunities, a ripple effect occurs, potentially casting a shadow over your credit score and credit utilization ratio.

When you approach a lender for new credit, they embark on a detective mission, leaving no stone unturned as they conduct a thorough investigation of your credit report. This process, known as a hard inquiry, holds the power to sway the tides of your credit scores, potentially bringing them down from their lofty heights.

So, try to steer clear of initiating any new credit applications near the time of making your mortgage application.

- Cultivation of Open Credit Accounts' Functionality

Bidding farewell to credit accounts can unleash a storm of negative consequences on your credit score and credit utilization ratio. By shrinking your available credit and inflating your credit utilization ratio, the act of closing accounts can send shockwaves through your financial standing.

Preserve the vitality of your credit history by leaving your credit accounts open, even in times of non-use. It's like safeguarding the roots of a healthy financial tree, ensuring a robust credit history for future growth.

- Credit Accounts' Blend

Blend the ingredients of your credit types in proper quantities to make them good enough to be called a balanced mix. Your portfolio of credit cards, personal loans, mortgages, and other forms of secured debts can give diversity to your profile, bringing a good impact on your financial standing. This in turn would enhance your application and help you in attaining your home financing and that too with good features.

Mix and match well to get the maximum gains.

- Credit Score Lookout

Along with the employment of strategies and keeping a check on the credit report and utilization ratio, being vigilant about the resultant rhythm of your credit score is essential too.

Harness the power of complimentary credit monitoring services like Credit Karma or Credit Sesame to effortlessly track your credit score and stay promptly informed of any noteworthy fluctuations.

Time Frame for an Improvement

The exact duration or time span to bring a boost in your credit score cannot be ascertained, as it is dependent on different factors and scenarios. What is certain is the fact that patience, effort, and consistency are very much required to wait for improvement.

You need to dig into what is or has brought a dip in your credit score and what is the right actionable strategy to adopt. For example, if you have delayed making a payment once, the drop in your credit score can easily be rectified by improving your payment schedules. But if you do not pay several dues on different accounts and that too for more than 90 days, your credit score would need days for recovery even after you clear the unpaid dues.

The time frame may vary in different circumstances. Most negative marks on your credit reports bid farewell after a period of seven years. It's like a magical vanishing act, where these blemishes lose their power to impact your credit scores. However, there's always an exception to the rule. Chapter 7 bankruptcies, like the stubborn outliers, can linger around for up to a decade, making their presence known long after other negatives have faded away. So, while most of the credit missteps take their leave, keep an eye out for those resilient bankruptcies that refuse to bow out until the ten-year mark.

So, basically, the point is you need to comprehend what and how your wrong financial moves are impacting your credit score and credit utilization ratio. With this clear understanding, you can rectify the situation accordingly.

You might come across credit repair companies promising to mend or "fix" your credit in exchange for a fee. It may sound alluring, but the truth is, these companies can't perform any magic tricks that you can't do yourself without spending a dime. Similarly, be cautious of debt settlement companies that urge you to halt payments in an attempt to hammer out a lower debt amount. Their strategy can inflict severe damage to your credit score and may not even succeed in reducing your overall debt obligation.

Bottom Line

By understanding and playing around with your current credit score and credit utilization ratio, you certainly can make your mortgage application strong. Not only this but you can also enjoy the additional perks of favorable interest rates and terms of your mortgage.

Implement and choose the right strategies and tricks to enhance your credit score and maintain the limits of your credit utilization ratio.

Seeking expert advice is always a wise recommendation. You can reach out to our affiliate members and get answers and relevant suggestions about credit score monitoring and mortgage application approvals.

FAQs

1. Why is your credit score crucial for a successful mortgage application?

This FAQ explains the significance of a strong credit score in the context of a mortgage application. It details how a good credit score demonstrates financial responsibility and the ability to repay debt, making it a major factor in mortgage eligibility.

2. What strategies can you use to boost your credit score for a mortgage application?

This FAQ explores various strategies for improving your credit score to enhance your mortgage application. It covers actions like checking your credit report for errors, paying bills on time, reducing debt, avoiding new credit applications, maintaining open credit accounts, and diversifying your credit mix.

3. How can you obtain your credit report for review, and why is it important to check for errors?

This FAQ provides information on accessing your credit report from the major credit bureaus and the importance of reviewing it for errors. It emphasizes the role of an accurate credit report in maintaining a healthy credit score.

4. How does paying bills on time impact your credit score, and what are some practical methods to ensure timely payments?

This FAQ discusses the significance of timely bill payments in maintaining a good credit score and provides practical methods for ensuring you pay your bills on time, including setting up automatic payments and reminders.

5. What is the credit utilization ratio, and how does it affect your credit score?

This FAQ defines the credit utilization ratio and explains its impact on credit scores. It emphasizes the importance of maintaining this ratio below 30% to improve your creditworthiness.