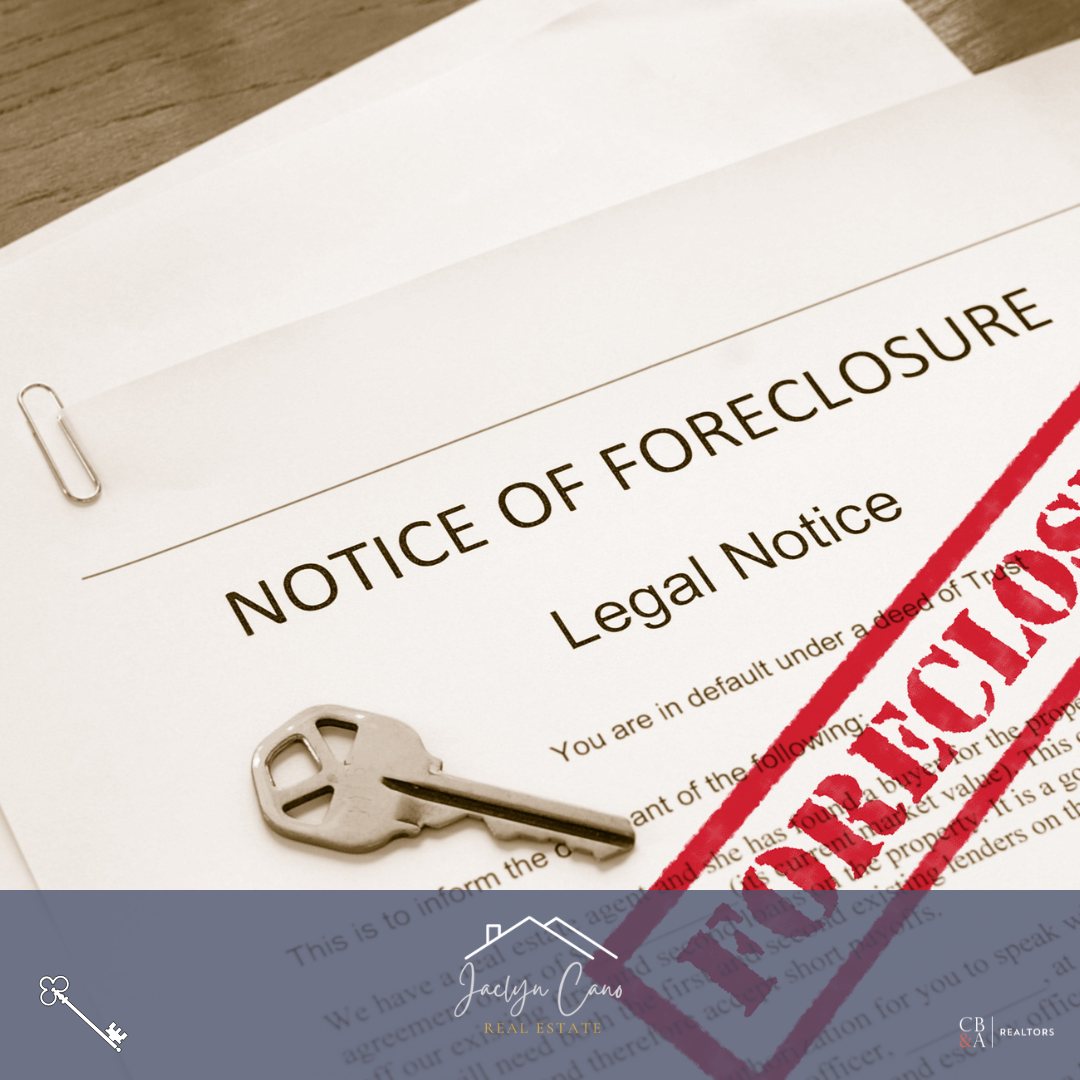

What Happens When the Foreclosure Process Starts in Texas

The real estate market over the last few years was on a whole new level. Market prices and rates were above average for a typical market season. Those who bought during this time have found themselves facing an uphill battle with their mortgage in today's current economy. Some buyer’s may very soon be facing the real possibility of being in distress. Distress is nothing to be ashamed of. However, if you or a family member are caught in distress I can give you a general idea of what happens when the foreclosure process starts in Texas.

Foreclosure Process

The foreclosure process in Texas is governed by state laws, and it typically follows a specific timeline and set of procedures. From the moment of default to closure Texas’s foreclosure process is that of about six months. Foreclosure process typically begins when a homeowner defaults on their mortgage payments. Here's an overview of what happens when the foreclosure process starts in Texas.

Missed Payments

The foreclosure process generally begins when a homeowner falls behind on their mortgage payments. Usually, after the first missed payment up to a few missed payments, the lender will send a Notice of Default and Acceleration to the borrower.

This notice will inform the borrower of the delinquent status of their loan and give them an opportunity to cure the default by bringing the loan current. I can’t stress this enough, if you are facing foreclosure or in a distressed situation please contact me. Real estate agents may be able to negotiate on your behalf to help keep you out of foreclosure. For more information on how I can help you check out my blog post on foreclosure in Texas.

Pre-Foreclosure Period

In Texas, there is typically a pre-foreclosure period during which the borrower can attempt to work out a solution with the lender, such as a loan modification, repayment plan, or short sale. Again, a real estate agent may be able to help with this process.

Texas identifies this process of missing a payment and pre-foreclosure period as NOD. Notice of Default (NOD): When a borrower misses mortgage payments, the lender may issue a Notice of Default. This document informs the borrower that they are in default and gives them a certain period to cure the default by paying the overdue amount.

Notice of Sale

If the borrower does not cure the default or work out an alternative arrangement such as short sale, pay off debt with the lender, the lender will file a Notice of Sale (NOS) in the county where the property is located.

This notice must be posted at the county courthouse and served to the borrower at least 21 days before the scheduled foreclosure sale. NOS notice includes details about the date, time, and location of the foreclosure sale. Along with being posted at the county courthouse Notice of Sale or NOS must be sent to the borrower. Thus begins the foreclosure sale process.

Foreclosure Sale

The foreclosure sale is typically a public auction held on the courthouse steps or another public location. It is conducted by the trustee or a substitute trustee appointed by the lender. The property is sold to the highest bidder, and the winning bidder must pay the bid amount in cash immediately or within a specified time frame. Once a home is placed into a foreclosure sale, at this point it will be difficult for a homeowner to remain in their property and continue to make payments on the home to reverse the default.

Right of Redemption

In some cases, Texas homeowners have a right of redemption or redemption period, allowing them to reclaim their property for a certain period after the foreclosure sale. A reclaiming of the property is done by paying the outstanding debt and associated or additional costs. The length of the redemption period may vary depending on the circumstances and the type of loan.

Eviction

If the homeowner does not redeem the property, the new owner (usually the lender or bank) can pursue eviction proceedings, if currently living in the property to take possession of the property. The exact process and timeline for eviction may vary based on local laws and court procedures.

Final thoughts

It's important to note that foreclosure laws and procedures can be complex, and the specific details may vary depending on the circumstances, the lender, bank, and any agreements or legal actions taken by the borrower. It is always recommended to consult with a real estate attorney when faced in a distressed situation. Borrowers facing foreclosure should seek legal advice and consider options to prevent or mitigate the foreclosure process, such as loan modification, short sale, or other loss mitigation options.

Additionally, it's essential to consult with a legal professional to fully understand the foreclosure process in Texas and how it may apply to a particular situation. Do consider checking for any updates or changes in Texas foreclosure laws, please do your research and if possible try to avoid the default process. As always, I’m here to answer any questions you may have and help you avoid the default process if possible. Contact me here at 346-573-4729 or realtorjaclyncano@gmail.com, I promise no judgment from me and only to share with you my expertise.