Sign In

Create an account and enjoy all the benefits of HAR.com!

Sign In

Sign in using social account

Fixed-Rate vs. Adjustable-Rate Mortgages: Choosing the Right Loan for You

Buying a home is exciting—but choosing the right mortgage is just as important as picking the perfect property. The two most common types of home loans are fixed-rate mortgages and adjustable-rate mortgages (ARMs). Each has its advantages and drawbacks, and the best choice depends on your financial situation and long-term plans.

Here’s a simple breakdown to help you navigate your options with confidence.

Fixed-Rate Mortgages: Stability You Can Count On

A fixed-rate mortgage offers a consistent interest rate for the entire loan term—whether it’s 15, 20, or 30 years.

Key Benefits:

? Predictable payments—Your monthly mortgage stays the same, making budgeting easier.

? Protection from rate increases—Even if interest rates go up, yours won’t change.

? Ideal for long-term homeowners—Best suited for those planning to stay put for many years.

Potential Downsides:

Slightly higher initial rates compared to ARMs.

Less flexibility—If rates drop in the future, you won’t automatically benefit.

Who Should Consider a Fixed-Rate Loan?

? Buyers who value stability and want to avoid surprises.

? Homeowners planning to stay in their property long-term.

? Budget-conscious individuals who prefer predictable monthly payments.

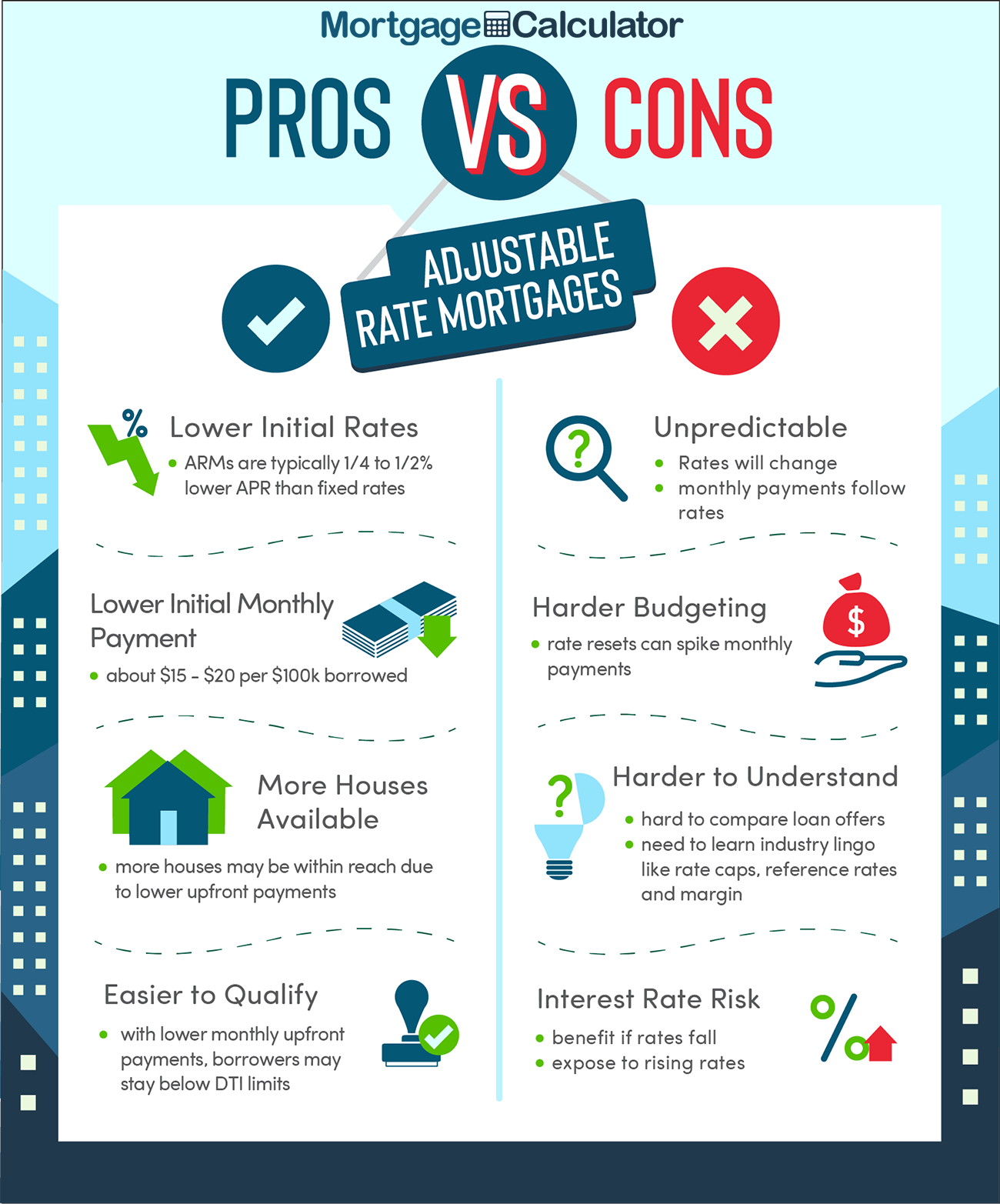

Adjustable-Rate Mortgages (ARMs): Short-Term Savings with Some Risk

An adjustable-rate mortgage (ARM) starts with a lower introductory interest rate for a set period (typically 3, 5, 7, or 10 years) before adjusting periodically based on market conditions.

Key Benefits:

? Lower initial rates—You’ll often start with a lower payment compared to a fixed-rate mortgage.

? Potential for future savings—If interest rates decrease, your rate (and payment) could go down.

Potential Risks:

Rates can increase after the introductory period, leading to higher payments.

Market-dependent—If rates rise significantly, your mortgage could become more expensive.

Who Should Consider an ARM?

? Short-term homeowners—If you plan to sell before the introductory period ends, an ARM can save you money.

? Flexible buyers—If you can handle payment fluctuations, this may be a good option.

? Strategic investors—If rates stay low, an ARM could be advantageous.

How to Choose the Right Mortgage for You

Your ideal mortgage depends on your financial goals, risk tolerance, and homeownership timeline. Ask yourself:

? How long do I plan to stay in my home?

? Do I need stable, predictable payments, or am I comfortable with rate changes?

? Can I handle an increase in payments if interest rates go up?

? Am I buying in a high-rate environment where a future refinance might be beneficial?

If you value stability, a fixed-rate mortgage is likely the best option. If you're buying short-term and want lower upfront costs, an ARM could be a smart choice.

Bottom Line

There’s no universal right answer—it depends on your situation. Consider your long-term financial goals, risk tolerance, and housing plans before making a decision. If you need guidance, consulting a trusted mortgage advisor can help you choose the best loan for your needs.

Would you like help comparing mortgage options based on your specific price range? Reach out to an expert today to make a confident, informed choice!

I'm Ryan with The Bridge Group

"Let's find a home you like"

(832) 621-5321

ryan@bridgegrouptx.com