Sign In

Create an account and enjoy all the benefits of HAR.com!

Sign In

Sign in using social account

Navigating Mortgage Rate Volatility: What You Can Control

If you’ve been paying attention to the housing market, you’ve likely noticed that mortgage rates fluctuate constantly. This kind of up-and-down volatility is normal when the economy is shifting—but it’s also frustrating.

Many buyers wonder whether they should wait for rates to drop before purchasing a home. But timing the market isn’t a guaranteed strategy—there’s no crystal ball that predicts exactly when rates will rise or fall.

The truth is, you can’t control the economy or mortgage rates, but you can take steps to set yourself up for the best possible deal. Even in an unpredictable market, factors like your credit score, loan type, and loan term are well within your control.

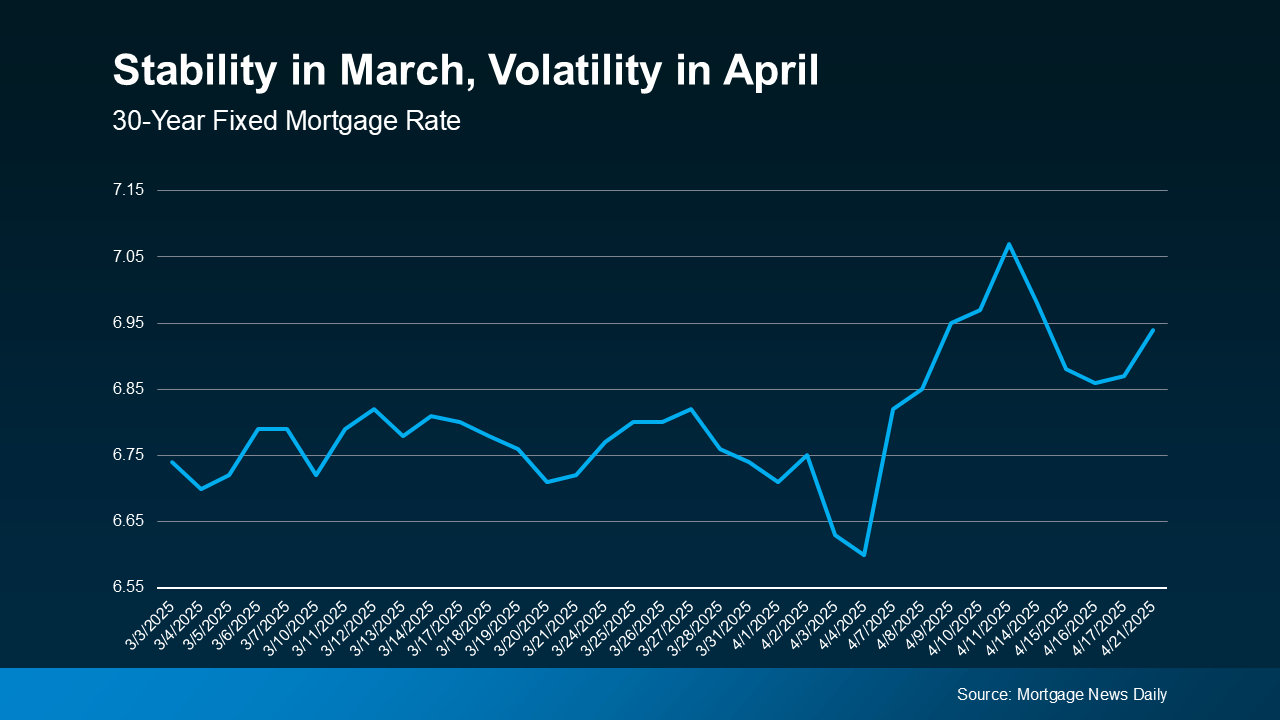

Take a look at the graph below. It uses data from Mortgage News Daily to show that after a relatively stable month of March, mortgage rates have been on a bit of a roller coaster ride in April:

Your Credit Score: The Key to Better Rates

Your credit score is one of the biggest factors that lenders consider when approving a mortgage. A strong score can make a huge difference in your interest rate—even small improvements can lead to significant savings over the life of the loan.

According to Bankrate:

"Your credit score is one of the most important factors lenders consider when you apply for a mortgage—not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for."

The takeaway? A better credit score means better mortgage terms. If you’re unsure about where your credit stands or how to improve it, consulting a loan officer can give you insight into what steps to take next.

Your Loan Type: Choosing What Works for You

Not all mortgages are created equal. The type of loan you choose can dramatically impact your interest rate and monthly payment.

The Consumer Financial Protection Bureau (CFPB) explains:

"There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements."

Each loan type has unique benefits and qualifications. That’s why working with a knowledgeable mortgage professional is essential—they can help you compare different options and find the one that aligns with your financial goals.

Your Loan Term: The Long-Game Strategy

Just like there are different loan types, there are also varied loan terms—typically ranging from 15, 20, or 30 years. Your loan term plays a big role in determining your:

? Interest rate

? Monthly payment amount

? Total interest paid over the life of the loan

Freddie Mac explains it best:

"When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home."

A shorter loan term usually means higher monthly payments but lower interest over time, while longer terms often come with lower monthly payments but more total interest paid. Your loan officer can help break down which option makes the most financial sense for you.

Bottom Line: Focus on What You Can Control

The economy and mortgage rates will continue to shift—but you don’t have to sit on the sidelines waiting for the perfect moment. By focusing on factors you can control—like your credit score, loan type, and loan term—you can position yourself for the best rate possible in today’s market.

The smartest move? Connect with a trusted real estate agent and lender now so you can take proactive steps toward homeownership—no matter where mortgage rates go next.

I'm Ryan with The Bridge Group

(832)621-5321

ryan@bridgegrouptx.com

"Let's find a home you like!"