Sign In

Create an account and enjoy all the benefits of HAR.com!

Sign In

Sign in using social account

Are you undecided about whether to sell your house? While affordability is showing signs of improvement this year, it's still tight, and this might be weighing on your mind. However, understanding your home equity could simplify your decision-making process. A Bankrate article explains:

"Home equity is the disparity between your home's current value and the outstanding balance on your mortgage. Essentially, it reflects the portion of your home that you've already paid for. You initially establish equity with your down payment when purchasing the home and continue to accrue it as you make mortgage payments. Additionally, as your home's value appreciates over time, your equity naturally increases."

Think of equity as a straightforward mathematical equation: it's your home's present value minus your outstanding mortgage balance. Interestingly, your equity has likely grown more than you realize in recent times due to the surge in home prices.

In the last few years, home values have soared, resulting in a corresponding increase in your home's value and, consequently, your equity. So, you might possess more equity than you previously thought.

How to Leverage Your Home Equity Effectively Now

If you're contemplating a move, the equity in your home could prove immensely beneficial. According to CoreLogic:

"...the average U.S. homeowner with a mortgage still has more than $300,000 in equity..."

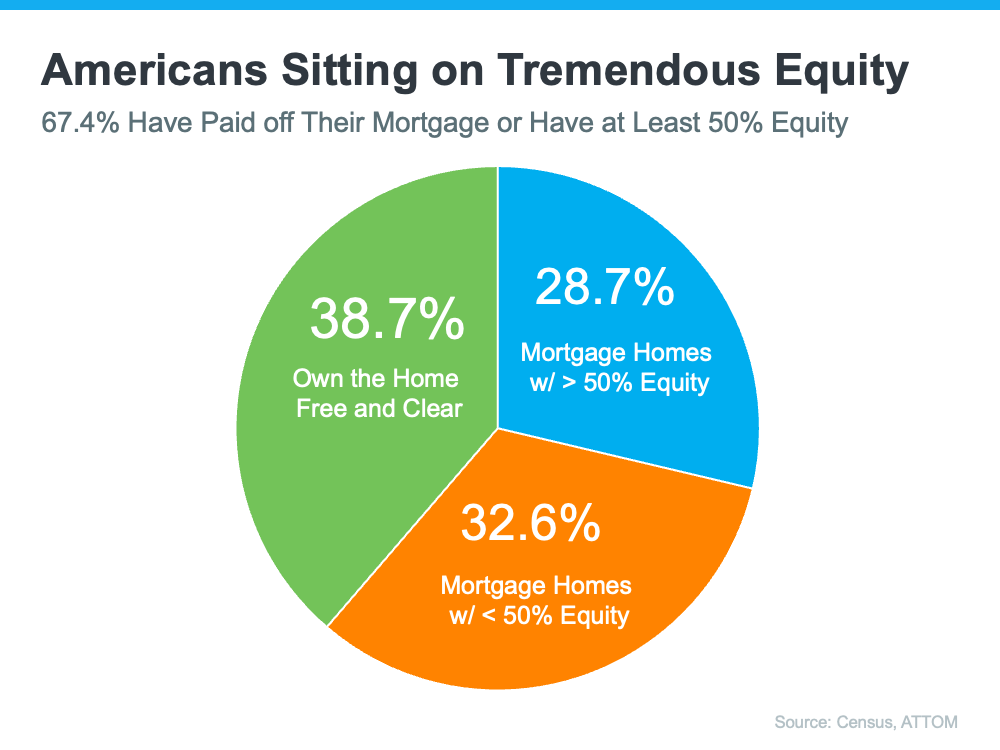

Evidently, homeowners currently hold significant equity. Recent data from the Census and ATTOM indicates that over two-thirds of homeowners have either fully paid off their mortgages or possess at least 50% equity.

This implies that roughly 70% of homeowners currently have a substantial amount of equity.

Once you sell your house, you can utilize your equity to facilitate the purchase of your next home. Here's how.

BECOME AN ALL CASH BUYER : If you've resided in your current home for an extended period, you might have accumulated enough equity to purchase your next home outright, without requiring a loan. In such a scenario, you wouldn't need to borrow money or worry about mortgage rates. As Investopedia suggests:

"You may want to pay cash for your home if you're shopping in a competitive housing market, or if you'd like to save money on mortgage interest. It could help you close a deal and beat out other buyers."

INCREASE YOUR DOWNPAYMENT: Your equity can also be allocated towards your next down payment. It might even be substantial enough to enable you to make a larger down payment, thereby reducing the amount you need to borrow. The Mortgage Reports explains:

"Borrowers who put down more money typically receive better interest rates from lenders. This is due to the fact that a larger down payment lowers the lender’s risk because the borrower has more equity in the home from the beginning."

The Convenient Method to Determine Your Equity

To ascertain the amount of equity you possess in your home, consider requesting a Professional Equity Assessment Report (PEAR) from a trusted real estate agent.https://markburgess.worthclark.com/