Sign In

Create an account and enjoy all the benefits of HAR.com!

Sign In

Sign in using social account

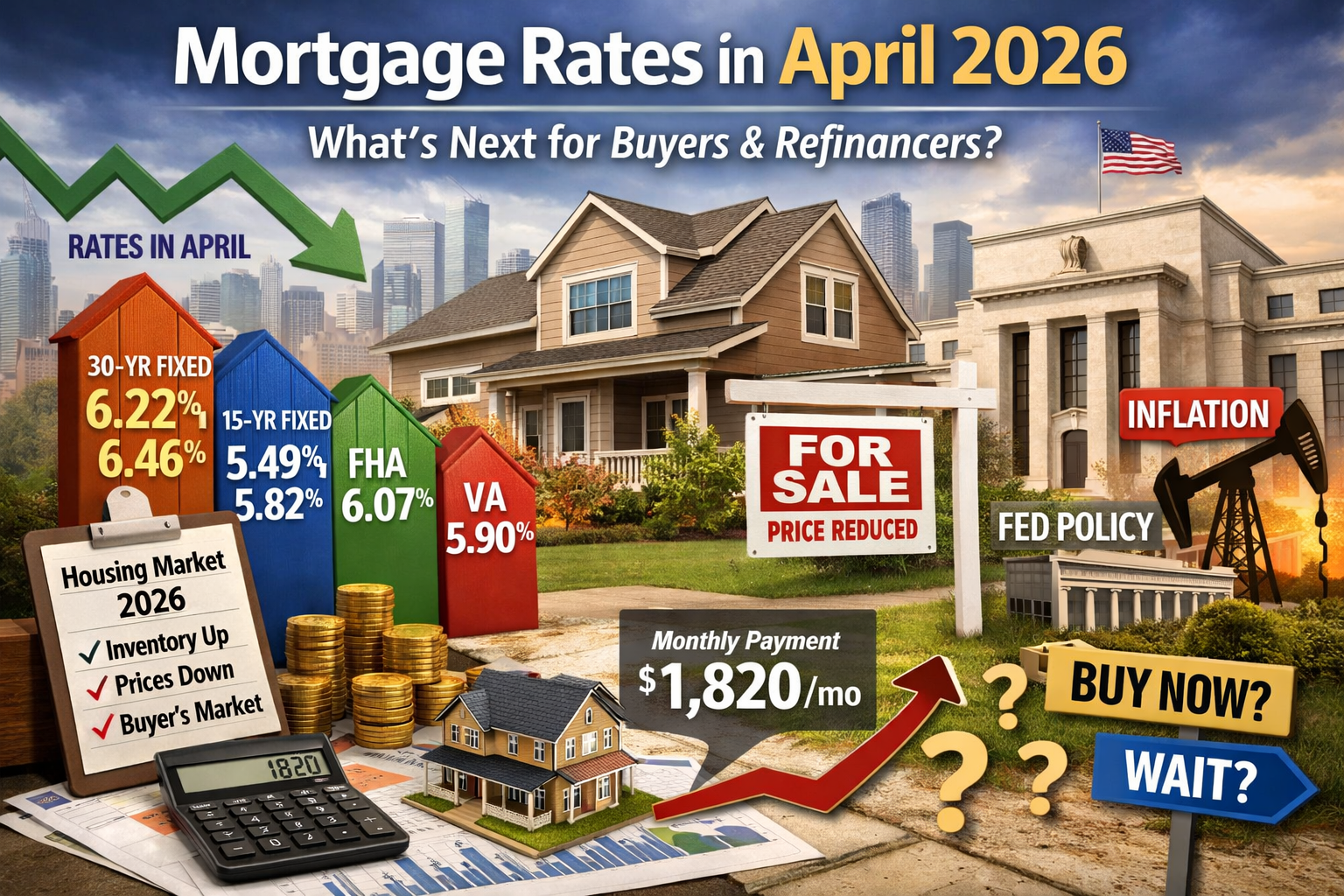

As spring 2026 unfolds, mortgage rates remain a critical factor for homebuyers and refinancers. With rates hovering around 6.22%-6.46% for 30-year fixed mortgages, understanding the current landscape and what experts predict can help you make informed decisions about timing your home purchase or refinance.

As of April 5, 2026, here's where rates stand across different loan types:

These rates represent a slight decline from early April, with the 30-year fixed dropping to 6.22% by April 5—a quarter-point decrease from the previous weekend. However, rates remain elevated compared to the pandemic-era lows of 2020-2021.

Several factors are influencing mortgage rates this spring:

1. Geopolitical Tensions and Inflation Concerns

Recent geopolitical events, including tensions in the Middle East, have raised energy costs and inflation concerns. This has pushed rates upward for five consecutive weeks, with the 30-year fixed climbing from 6.38% to 6.46% in early April.

2. Economic Data and Fed Policy

The Federal Reserve's cautious stance on rate cuts continues to influence mortgage rates. While the Fed hasn't raised rates, the lack of aggressive cuts has kept mortgage rates stable in the 6%-6.5% range.

3. Seasonal Spring Demand

Spring is traditionally the busiest homebuying season, and increased demand for mortgages can put upward pressure on rates. However, rising inventory is tempering some of this pressure.

Monthly Payment Comparison

For a $300,000 loan at current rates:

Affordability Advantage

Despite rates hovering around 6%, affordability is improving compared to 2025. Here's why:

This combination means that even at 6.22% rates, buyers have more purchasing power than they did a year ago.

Reasons to Buy Now:

Reasons to Wait:

The Bottom Line: If you're ready to buy and have found a home you love, current conditions favor buyers. The combination of lower prices, rising inventory, and stable rates creates a window of opportunity. Waiting for rates to drop further could mean missing out on better prices and more inventory.