Sign In

Create an account and enjoy all the benefits of HAR.com!

Sign In

Sign in using social account

For the past few years, the real estate market has felt like a game of musical chairs where the music never stops, but the chairs are bolted to the floor. High interest rates and record-low inventory created a "lock-in effect" that kept homeowners from selling and buyers from entering the arena. But as we move into mid-January 2026, the music is finally changing.

The headline for 2026 is simple: The Unlock. With mortgage rates projected to average 6.3% and potentially dip toward the 6% mark by year-end, we are witnessing a massive shift in market dynamics. According to recent data from the National Association of Realtors (NAR), a single percentage-point drop in mortgage rates can expand the pool of qualified buyers by approximately 5.5 million households.

Why is 6% such a magic number? For many, it’s the psychological and financial tipping point. At 7% or 8%, the monthly debt-to-income ratio for the average American family was stretched to its breaking point. At 6.3%, the math starts to work again.

Consider this: On a $400,000 mortgage, the difference between a 7.5% rate and a 6.3% rate is roughly $300 per month. Over the life of a 30-year loan, that’s over $100,000 in interest savings. This "extra" money isn't just a luxury; for 1.6 million renters currently on the sidelines, it is the difference between a "denied" and an "approved" mortgage application.

Lower rates don't just help buyers; they incentivize sellers. Many homeowners who have been "locked in" to 3% or 4% rates are finally deciding that the gap between their current rate and a new 6% rate is manageable.

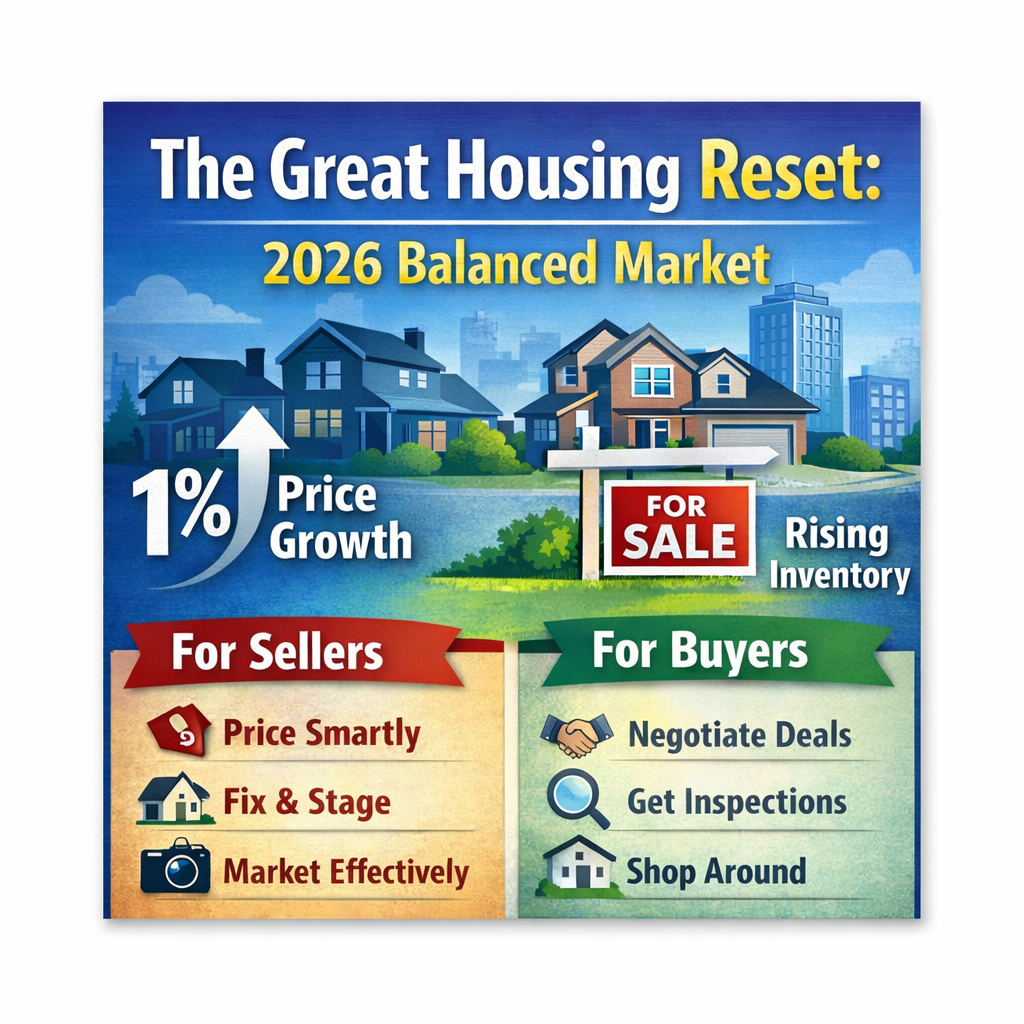

Active listings are projected to increase by 8.9% in 2026. While we are still about 12% below pre-pandemic inventory levels, the trend is undeniably positive. For a buyer, this means more choices, fewer bidding wars, and—most importantly—the return of the inspection contingency.

2026 isn't about a market crash; it's about a market reset. The "Unlock" is providing a window of opportunity for those who have been patient. As affordability improves and inventory grows, the power is slowly shifting back into the hands of the consumer.